Bangladesh’s readymade garment sector is entering a decisive phase as United States fashion companies accelerate a restructuring of their global sourcing strategies in response to rising tariffs, geopolitical tensions and an uncertain consumer environment, according to a new academic study.

The research, titled “U.S. Fashion Companies’ Evolving Sourcing Practices amid Tariffs and Geopolitical Tensions”, was conducted by Sheng Lu of the University of Delaware and draws on a thematic analysis of earnings call transcripts from around 30 leading publicly listed American fashion companies between February and April 2026, providing a clear snapshot of evolving global sourcing patterns in the apparel industry.

The study indicates a significant rebalancing of supply chains that could reinforce Bangladesh’s position as one of the world’s leading apparel exporters, despite ongoing uncertainties facing the industry.

At the core of this shift is a convergence of economic and policy pressures. US fashion companies identified weakening consumer demand, macroeconomic volatility, tariff hikes and ongoing policy uncertainty as their most pressing concerns.

The strain on middle- and lower-income consumers in the United States has become particularly pronounced, with many retailers reporting that these groups are increasingly cautious in discretionary spending.

The study found that a convergence of economic and policy pressures was driving this shift, with US fashion companies identifying weakening consumer demand, macroeconomic volatility, tariff hikes and ongoing policy uncertainty as their most pressing concerns.

It noted that the strain on middle- and lower-income consumers in the United States had become more pronounced, with retailers observing that these groups were increasingly cautious in discretionary spending.

According to the report, major retailers such as Kohl’s and Macy’s pointed to diverging performance trends, indicating that higher-income consumers remained relatively resilient while lower-income shoppers continued to cut back.

Companies including Carter’s and Oxford Industries were said to have highlighted the difficulty of forecasting demand amid mixed economic signals, including subdued consumer confidence and persistent inflation.

Tariffs were described as a dominant factor shaping business strategies. In response, many brands were reported to be relying increasingly on selective price increases and a shift towards full-price selling to protect margins.

The study found that companies were raising prices mainly on fashion-forward and premium items while keeping core and basic products affordable to retain price-sensitive customers.

Brands such as Columbia Sportswear and Levi Strauss & Co. were reported to have implemented mid- to high-single-digit price increases, supported by product innovation and tighter cost control.

Several companies indicated that consumers had shown little resistance to these adjustments, allowing retailers to partially offset tariff-related costs.

At the same time, firms were said to be scaling back promotional campaigns to encourage full-price sales.

Victoria’s Secret was reported to have achieved improved margins driven by reduced discounting and higher average selling prices, reflecting a broader trend towards restoring pricing discipline.

While pricing strategies were evolving, the study indicated that the most consequential changes were taking place in sourcing decisions. It identified four key strategies shaping global apparel production.

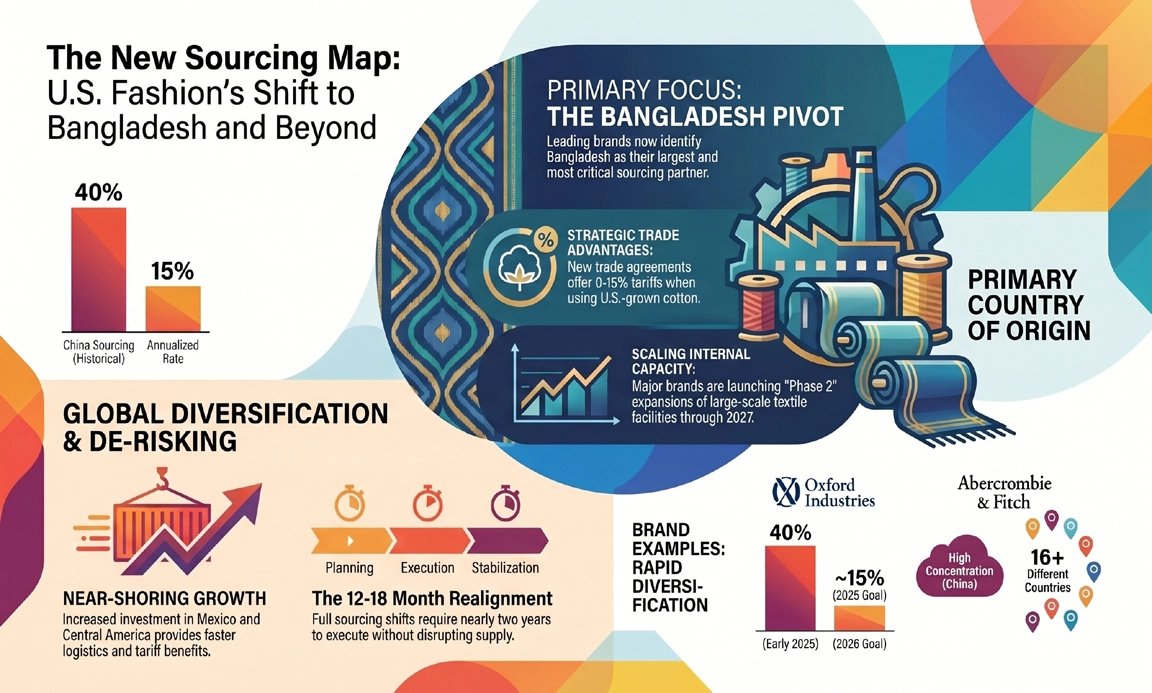

First, companies were reported to be accelerating diversification away from China, a process that had gained urgency amid tariff pressures and geopolitical risks.

Second, there was a clear shift towards expanding sourcing from lower-cost Asian hubs, particularly Bangladesh and Vietnam, with Bangladesh emerging as a major beneficiary due to its scale, cost competitiveness and established manufacturing base.

Several companies noted that Bangladesh had become their largest sourcing destination.

Kontoor Brands was reported to have highlighted that the country accounted for the bulk of its sourcing volume, making it both a critical partner and a focal point for tariff exposure.

Third, companies were said to be exploring near-shoring options in Mexico and Central America to shorten lead times and benefit from preferential tariff arrangements, although this trend was not expected to replace Asian sourcing due to cost and capacity constraints.

Fourth, the study noted that companies were closely monitoring evolving trade agreements, particularly those involving Bangladesh.

A recently signed reciprocal tariff arrangement between Bangladesh and the United States was reported to have reduced tariffs on Bangladeshi products from 20 per cent to 19 per cent, while offering duty-free access for garments produced using US-origin cotton and man-made fibres.

This provision was said to have attracted significant attention from buyers, with companies increasingly factoring such trade frameworks into sourcing decisions where tariff savings could be achieved through compliance with input requirements.

Executives were reported to have stressed that supply chain realignment was a gradual process, typically taking between 12 and 18 months or longer, suggesting that the current shift towards Bangladesh and other Asian sourcing hubs would likely continue over the medium term.

Investment trends were also said to reflect this outlook. Gildan was reported to have announced plans to expand its industrial footprint in Bangladesh, including the construction of a second large-scale textile facility expected to begin production in 2027, underscoring confidence in the country’s long-term role as a strategic manufacturing base.

At the same time, companies were said to be maintaining flexibility by diversifying sourcing across multiple regions, including India and Central America, to mitigate risks and respond to changing market conditions.

Geopolitical tensions remained a key concern. Although conflicts in regions such as the Middle East had not significantly disrupted sourcing operations, companies were reported to be closely monitoring indirect impacts on logistics and shipping.

Brands including Nike and PVH Corp were said to have experienced some delays linked to regional instability, although these had remained manageable.

Industry stakeholders in Bangladesh acknowledged both the opportunities and challenges arising from these shifts.

Leaders of the Bangladesh Garment Manufacturers and Exporters Association were reported to have emphasised the need for a clear mechanism to verify the use of US cotton in garments so that exporters could fully benefit from tariff concessions.

Shovon Islam, managing director of Sparrow Group, was reported to have said that buyers remained actively engaged with Bangladesh, although decision-making had slowed due to geopolitical developments and policy uncertainties.

He added that both buyers and suppliers were working together to adapt to the evolving landscape.

At the policy level, industry players were said to be urging the government to negotiate more favourable terms, including the possibility of zero-duty access for garments produced using US cotton, in order to strengthen Bangladesh’s competitive position.

The study ultimately portrayed a global apparel industry in transition, where resilience, flexibility and supply chain agility were becoming as important as cost efficiency.

For Bangladesh, the evolving landscape was seen as presenting a significant opportunity to deepen its role in global sourcing networks, although sustaining this momentum would require careful navigation of external risks, continued investment in capacity and compliance, and proactive engagement with changing trade and market dynamics.