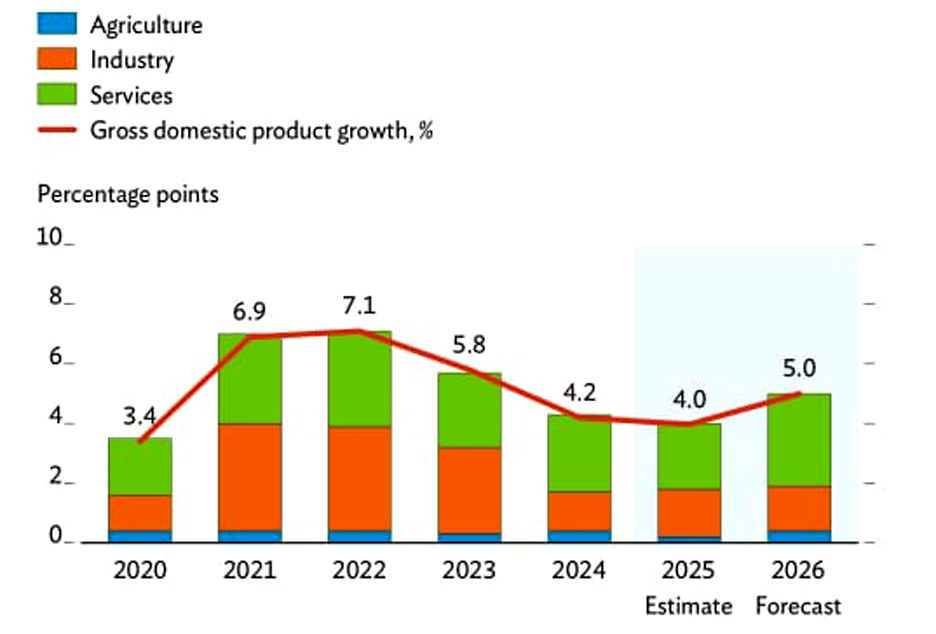

Bangladesh’s economy is projected to regain momentum in the next financial year, with gross domestic product (GDP) growth forecast to rise from 4.0 per cent in FY2024–25 to 5.0 per cent in FY2025–26, according to the Asian Development Outlook (ADO) September 2025 released by the Asian Development Bank (ADB).

The estimate followed a 4.2 per cent expansion in FY2023–24 and reflected a gradual recovery despite persistent structural and external challenges.

The ADB report, released on September 30, observed that garment exports continued to show resilience, yet broader growth in FY2025 was restrained by political uncertainty, recurrent flooding, labour disputes, and stubbornly high inflation.

Growth, which stood at only 2.0 per cent in the first quarter of FY2025, improved to 4.5 per cent in the second quarter and 4.9 per cent in the third, driven largely by manufacturing.

Consumption and investment showed modest gains, supported by remittances, but were curtailed by tight fiscal and monetary conditions.

ADB Country Director for Bangladesh, Hoe Yun Jeong, underscored the importance of structural reforms in securing stronger growth.

‘Future growth will depend on improving the business environment to boost competitiveness and attract investment, and on ensuring reliable energy supplies,’ he said.

He said that the impact of US tariffs on Bangladesh’s trade was yet to be seen and that vulnerabilities in the banking sector persisted, adding that addressing these challenges was essential to achieving higher economic performance.

ADB Country Director said that some downside risks to the FY2026 outlook remained, explaining that trade uncertainty, banking sector weaknesses, and potential policy slippages could impede progress.

He stressed that maintaining prudent macroeconomic policies and accelerating structural reforms were critical to strengthening resilience.

According to the ADB report, inflation remained a central concern, having risen from 9.7 per cent in FY2024 to a projected 10.0 per cent in FY2025.

The report stated that price pressures were the result of supply chain constraints, insufficient market competition, and depreciation of the taka.

Inflation was expected to ease to 8.0 per cent in FY2026, provided that favourable weather, stable global oil prices, and tighter domestic policies were in place.

It said that Bangladesh Bank had held its repo rate at 10.0 per cent since October 2024 and was likely to maintain this stance until headline inflation fell significantly.

The ADB observed that external sector indicators showed some improvement, with the current account moving from a deficit of 1.5 per cent of GDP in FY2024 to a small surplus of 0.03 per cent in FY2025, largely due to record remittance inflows.

It noted that official transfers had reached $30.3 billion, a 26.8 per cent increase year-on-year, supported by a competitive exchange rate and government incentives.

Foreign exchange reserves, it stated, rose by $6 billion to $26.7 billion, covering 4.2 months of imports.

However, the report projected that for FY2026 the current account would return to a small deficit of 0.08 per cent of GDP.

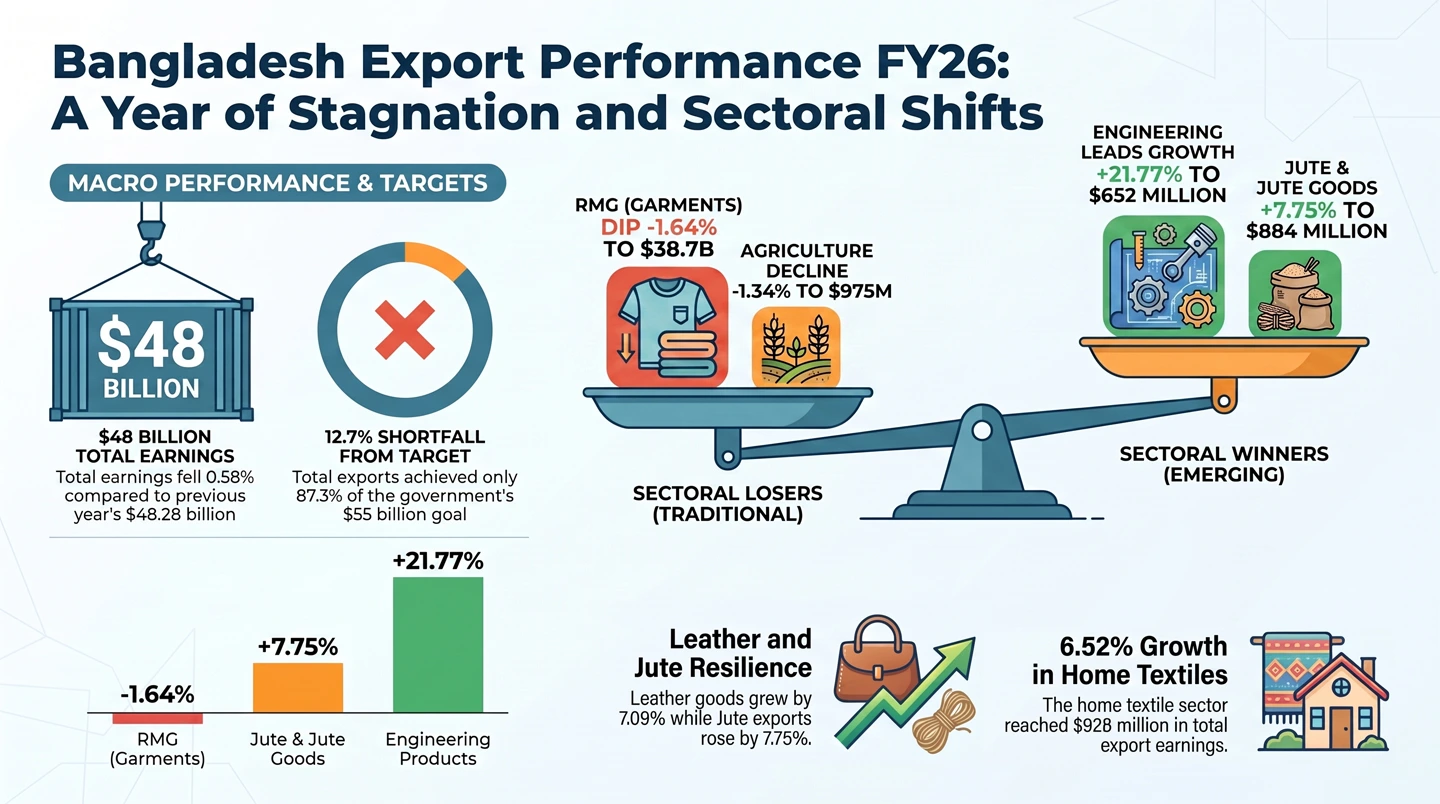

The report further pointed out that the external trade environment posed significant risks. It highlighted that Bangladesh’s exports had grown by 7.7 per cent in FY2025, reversing a decline the previous year thanks to competitive pricing and cash incentives.

However, it said that from August 2025 the United States had imposed a 20 per cent tariff on Bangladeshi exports, raising average duties from 15 per cent to 35 per cent.

Apparel, which accounts for the bulk of shipments, saw tariffs rise from 16.8 per cent to 36.8 per cent, with some items facing duties as high as 52 per cent.

As nearly one-fifth of Bangladesh’s exports were destined for the US, the ADB cautioned that the impact could be severe, potentially forcing exporters to lower prices or seek alternative markets, especially in the European Union where competition was already intensifying.

On the supply side, the ADB projected that services would benefit in FY2026 from rising household purchasing power, while agriculture was expected to stabilise if supported by favourable weather and effective policy.

In contrast, it anticipated that industrial growth might slow due to new trade barriers.

It also forecast that consumption—both private and public—would be the main driver of growth, bolstered by remittance inflows and election-related spending. Investment, however, was expected to remain subdued as a result of tight monetary conditions and investor caution.

The ADB stressed that fiscal pressures would remain a challenge, noting that interest payments had consumed nearly a fifth of government revenues in 2024.

It stated that while the FY2025 budget deficit was targeted at 4.1 per cent of GDP, the figure might overshoot given slower-than-expected revenue collection.

Money supply growth, it added, had slowed to 7.0 per cent in FY2025, reflecting a cautious policy stance.

The report warned that several downside risks could undermine the FY2026 outlook, including uncertainties over trade policies, weaknesses in the banking sector, poor implementation of the new exchange rate regime, election-related spending pressures, and climate shocks.

It cautioned that any slippage in fiscal and monetary discipline could intensify inflationary pressures and worsen external imbalances.

Nonetheless, the ADB maintained that Bangladesh retained strong fundamentals, citing its large workforce, robust remittances, and competitive export sectors.

It said that with disciplined policies and reforms to improve governance, strengthen infrastructure, and diversify markets, the country could position itself for stronger and more resilient growth in the medium term.